A firm must decide whether to distribute all profits, retain them, or distribute a portion and retain the balance. Dividend decision is essentially a trade-off between retained earnings and issue of new shares. Dividend decision model helps a firm to make a profitable choice between the two.

Dividend decision consists of two important theories which are based on the relationship between dividend decision and value of the firm.

- Relevance Theory of Dividend – Walter`s model, Gordon`s Model

- Irrelevance Theory of Dividend – Modigliani and Miller`s Approach

Relevance Theory –

According to this theory, the dividend decision of a firm affects the market value of the firm. It suggests that shareholders prefer current dividend and there is a direct relationship between dividend decision and value of the firm. This theory was supported by two professors James E. Walter and Myron Gordon.

Walter`s Dividend Decision Model –

According to this approach dividend decision is an active variable that influences share price and value of the firm. James E. Walter believed that the dividend decision of a firm always affects the market value of the firm.

In determining the significance of dividend decisions Walter related the firm’s Internal Rate of return (r) with the firm`s Cost of capital (Ke).

According to Walter –

- If r > Ke – The firm should retain its earnings.

- If r < Ke – The firm should distribute its earnings so that shareholders can make higher earnings by investing elsewhere.

- If r = Ke – The firm can be indifferent towards earnings retained or distributed

Based on the relationship between a firm`s Ke and r there may be the following types of firms –

Growth Firms- [r>k] – These firms have ample investment opportunities promising high rate of return in the future. Therefore they should retain earnings to grow more and must not distribute any dividend.

Declining Firms – [r<k] – These firms lack investment opportunity and therefore it should distribute all its earnings so that the investors can invest it elsewhere and earn better return.

Normal firms – [r=k] – In these firms shareholders are indifferent between retention and distribution of earnings as the firm does not have the ability to earn huge profits in near future.

According to this dividend decision model, if a firm has a return on investment greater than its cost of equity capital, then it must prefer high dividend payout ratio in order to maximize its market value.

Assumptions of Walter Model –

- The firm does not use debt or equity financing.

- Retained earnings are the exclusive source of financing.

- The Firm`s (r) and (Ke) are constant.

- The Firm either entirely distributes or retains its earnings.

- There is no change in earning per share and dividend distributed.

- The firm has a perpetual life.

- Corporate taxes do not exist.

Determining the Market Value of Shares According to Walter`s Approach

According to Walter Model of Dividend decision Market Value of Share is the sum of the market value of two sources of income.

- Present Value of all dividends = D/Ke and,

- Present Value of all capital gains = [r(E-D)Ke]/Ke

Therefore,

P = D/Ke + [r (E-D)/Ke]/Ke

Where,

P = Market price per share

D = Dividend Per Share

E = Earnings Per Share

R = Internal rate of Return

Ke = Cost of Capital

Criticism of Walter`s Dividend decision Model

It has been criticised on the following points:

- It assumes that there is no external financing used by the firm which is not practical.

- It assumes constant return which cannot be possible.

- It assumes constant cost of equity capital which is not practical as every business faces uncertainties.

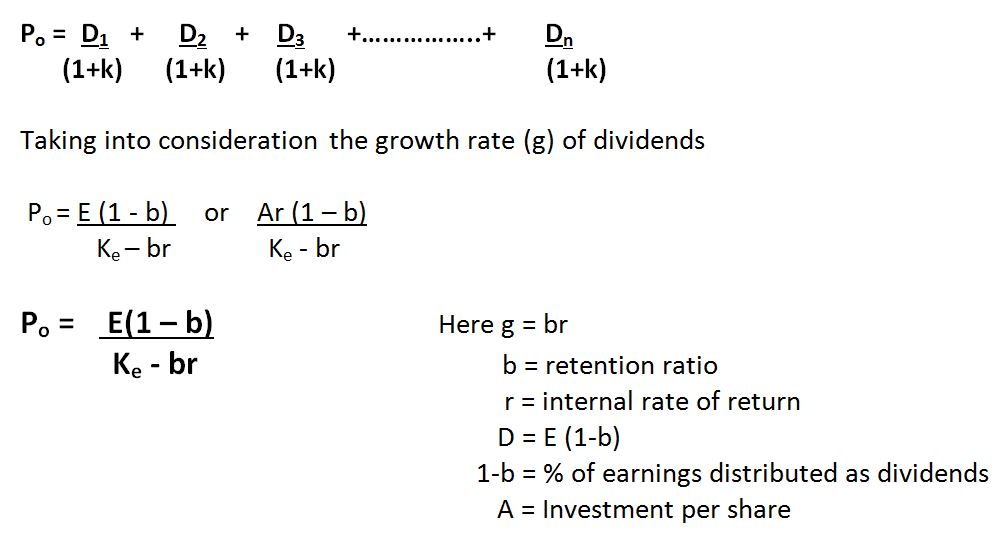

Gordon Dividend Decision Model

Gordon argued for the relevance of dividend decisions to valuation of firm. He believed that investors or shareholders prefer current dividends to future dividends as they are rational and not committed to take risks.

Payment of current dividends completely removes the possibility of risk. This is why when a firm retains its earnings its value receives a setback.

According to him preference for dividend exists even if r = Ke (Contrary to Walter)

Gordon`s dividend decision model is also known as Dividend Equalization Model

Assumptions of Gorden Model-

- It is an all equity firm

- The Firm`s (r) and (Ke) are constant.

- The firm has a perpetual life.

- Corporate taxes do not exist.

- Retention Ratio once decided remains constant. Thus, growth rate (g = br) is constant.

- ‘K’ is greater than ‘Br’ which is equal to ‘g’ (K>br=g). It is an essential condition to get a meaningful value of share.

Determining the Market Value of Shares According to Gordon`s Approach

According to Gordon the Market Value of Share (P) of a firm is equal to the Present Value of all the dividends to be received by the shareholders in the future.

Criticisms of Gordon`s Model

It has been criticised on the following points:

- Gordon model assumes that there is no debt and equity finance used by the firm, which is not applicable to present day business.

- Ke and r cannot be constant in the real practice.

Irrelevance Theory –

Modigliani and Miller’s Approach –

According to Modigliani and Miller dividend decision model, under a perfect market condition, dividend decision has no effect on the share price of the company and that there is no relation between the dividend rate and market value of the shares. Therefore dividend decision is irrelevant factor does not affect the value of the firm.

Assumptions

- There is a perfect capital market.

- All Investors are rational.

- Government does not impose any taxes.

- The firm has fixed investment policy.

- There are No risk or uncertainty factors.

Determining the Market Value of Shares According to Modigliani and Miller’s dividend decision model

According to this dividend decision model market value of a share can be found out by the following –

1) Calculate the prevailing market price of share –

Po = D1 + P1

(1 + Ke)

Where,

Po = Prevailing market price of a share.

Ke = Cost of equity capital.

D1 = Dividend to be received at the end of period one.

P1 = Market price of the share at the end of period one.

2) Compute the value of P1(market value of share) by the following formula =

P1 = Po (1+Ke) – D1

3) If the company needs to issue fresh shares in order to meet its investment needs. Gordon gave the formula to find out the number of new shares to be issued.

New Shares to be Issued = I – (E – nD1)

P1

Where,

P1 = Price of new issue

I = Amount of investment required

E = Total Earnings/ Total Net Profit of the firm during that period.

nD1 = Total dividend paid during that period.

Now the value of the firm can be calculated as under:

nPo = (n+m)P1 – (I-E)

1 + Ke

n = No. of shares outstanding at the beginning of the period.

Criticism of Modigliani and Miller’s dividend decision model

It has been criticised on the following points:

- It does not consider taxes.

- It does not consider risks and uncertainty associated with a business.

- It does not consider flotation and transaction cost.

- Investors do not always behave rationally.

- It poses difficulty in the diversification plans of the firm.